In this blog post, we'll cover:

- How CCP2 Works

- CPP and CPP2 Contribution Rates & Maximums

- Calculating CPP2 Payroll Deductions

- The Effects of the Canada Pension Plan Enhancement

- Important Resources Moving Forward

How Does CPP2 Work?

First CPP Contributions

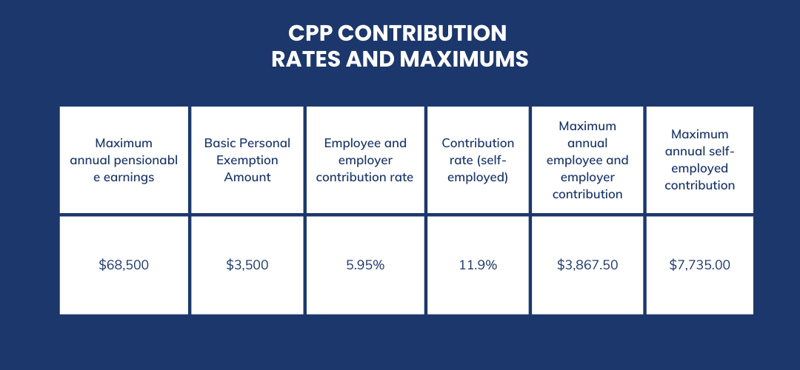

The Canadian Pension Plan (CPP) is a mandatory deduction for all Canadian workers who are between the ages of 18-65 and it is a core component of Canada's retirement ecosystem. Employers have the responsibility of deducting and remitting their employees' CPP contributions. The basic CPP exemption amount remains $3,500 in 2024. Employers must match their employees' contributions at a rate of 5.95% in 2024, up to a maximum contribution of $3,867.50 each. For self-employed individuals, the contribution rate includes the combined rates of both the employee and employer, totaling 11.9% in 2024 up to a maximum contribution amount of $7,735.00.

CPP2 Contributions

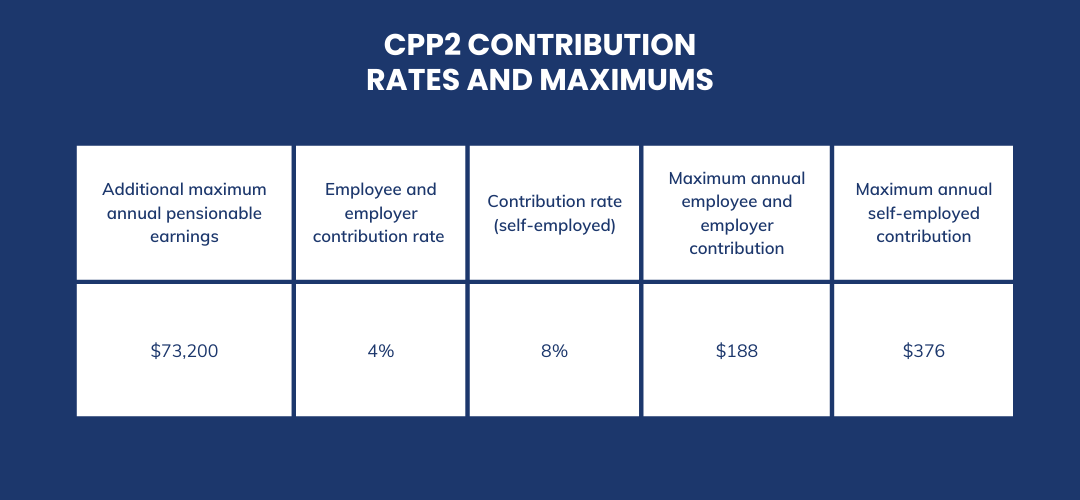

Beginning on January 1, 2024, there will be enhanced CPP contributions for workers earning higher wages, known as CPP2. These contributions are made in addition to the first CPP. Workers earning annual wages over the first maximum pensionable earnings ceiling of $68,500 will make second CPP contributions up to the second maximum pensionable earnings ceiling of $73,200. The employer/employee rate for CPP2 contributions is 4% in 2024, while the self-employed rate is set at 8%. The CPP2 maximum contribution limit is $188 for employees and $376 for self-employed individuals annually (refer to figures 1 & 2 for further details).

According to the CRA, if employees earn more than the first earning ceiling, but less than the second earning ceiling:

They will contribute 4% of the amount they earn that is above the first earning ceiling. Their employers will also contribute 4% on their behalf.

Self-employed individuals who earn more than the first earning ceiling, but less than the second earning ceiling, will contribute 8% of the amount they earn that is above the first earning ceiling.

If you earn less than the first earning ceiling, you will not make CPP2 contributions.

CPP and CPP2 Contribution Rate Maximums

Calculating CPP2 Payroll Deductions

With the above information serving as our basis for calculating CPP2, let’s break it down with an example:

- Example One: Eric works as an executive and makes $130,000 a year on a bi-weekly payroll frequency (26 pay periods). Let’s calculate Eric’s CPP and CPP2 contributions per pay period:

Calculating Base CPP Per Pay Period

Step one: Calculate the basic pay period exemption: divide the basic yearly exemption of $3,500 by the number of pay periods.

$3,500 ÷ 26 pay periods = $134.61

Step two: Calculate total pensionable income for this pay period, which equals the sum of gross pay, up to a maximum of $68,500, divided by the number of pay periods.

$68,500 ÷ 26 pay periods = $2,634.61

Step three: Deduct the basic exemption amount from step one from the total pensionable income from step 2:

$2,634.61 - $134.61 = $2,500

Step four: Calculate the amount of CPP contributions by multiplying the total from step three by the CPP contribution rate (5.95%):

$2,500 x 0.0595 (5.95%) = $148.75

Total CPP contribution per pay period for Eric: $148.75

Calculating CPP2 Per Pay Period

Step one: Calculate the total pensionable income above the first earning ceiling up to the second earning ceiling and divide it by the number of pay periods.

$73,200 - $68,500 ÷ 26 = $180.70

Step two: Calculate the amount of CPP2 contributions by multiplying the total from step one by the CPP contribution rate (4%):

$180.70 x 0.04 (4%) = $7.23

Total CPP2 contribution per pay period for Eric: $7.23

Calculate Annual CPP & CPP2 Contributions

Rather than calculating on a per pay period basis, lets look at the calculation of Eric’s annual CPP and CPP2 contributions:

Step one: Calculate Eric’s base CPP contributions by subtracting the basic personal exemption amount ($3,500) from the maximum pensionable earnings amount ($68,500) and multiplying by the CPP contribution rate of 5.95%

$68,500 - $3,500 x 0.0595 (5%) = $3, 867.50

Total annual CPP contribution: $3, 867.50

Step two: Next, because Eric earns more than the second earnings ceiling, we will take the second earnings ceiling and subtract the first earnings ceiling and multiply this amount by the CPP2 contribution rate of 4%.

$73,200 - $68,500 x 0.04 (4%) = $188.00

Total annual CPP2 contribution: $188.00

Understanding the Effects of CPP2

Changes to T4 Slips Following CPP2 Enhancement

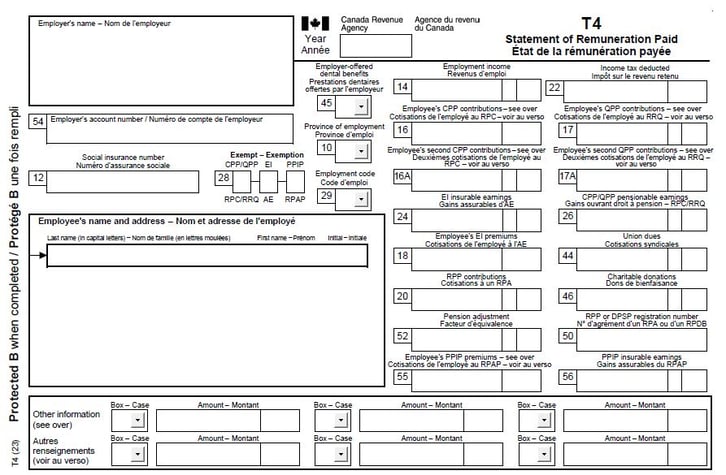

Due to the recent CPP enhancement, the CRA has introduced new boxes on the T4 slip specifically for reporting the second CPP contribution. Employers will now utilize the following additional boxes: 16A for the employee's second CPP contributions, and 17A for the employee's second QPP contributions.

The Canada Revenue Agency has advised that since this is effective for January 1, 2024, boxes 16A and 17A will be left blank for 2023 tax year.

Don’t want to deal with these new calculations, filing changes and continued adjustments to CPP deductions moving forward? Let us take care of it for you.

Increased Retirement Benefits

One of the most notable enhancements of CPP2 is the increase in retirement benefits. This is positive news for those planning for their retirement years, as it means a larger source of income from the CPP. The CPP2 enhancement aims to gradually raise the income replacement rate from the current 25% to 33.33% of eligible earnings. This increase is designed to help Canadians maintain their standard of living during retirement, especially in a time when the cost of living continues to rise. This enhancement to the Canada Pension Plan will have the greatest impact on young Canadians entering the workforce.

Survivor's Benefits

CPP2 aims to strengthen survivor's benefits as well, providing greater financial protection to the surviving spouse or common-law partner of a deceased contributor. The survivor's pension will increase to 75% of the deceased contributor's pension, up from the current 60%. This change ensures that those left behind will have a more substantial source of income after the loss of a loved one, offering greater peace of mind during a challenging time.

Disability Benefits Enhancement

For those who become disabled and unable to work, CPP2 will also bring enhancements to disability benefits. The enhancement aims to provide more comprehensive support to individuals facing disabilities, ensuring they have access to the financial resources they need to maintain their quality of life.

Important CPP Resources Moving Forward

As CPP2 rolls out, it's vital for Canadians to understand the intricacies of the plan. Knowing how to calculate and deduct CPP2 contributions is key. With varying earning ceilings and contribution rates, individuals and employers need to comprehend their obligations regarding contributions, ensuring compliance with the new regulations.

The availability of vital resources, such as PayTrak’s 2024 Payroll Guide and the CRA’s CPP2 Resource Page linked below, will play a pivotal role in aiding individuals and businesses in navigating these changes seamlessly. Accessing these resources and understanding Canadian payroll deductions will be instrumental in staying compliant and well-informed regarding CPP2.

For more information about statutory deductions and remittances, visit our blog post Understanding Payroll Deductions and Remittances in Canada.

We recommend downloading our Payroll Guide for more information on upcoming changes to payroll legislation. You can access additional information through the links below.

.png?width=352&name=Workers%20Comp%20Blog%20(1).png)